Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

COMING SOON: CHANGES TO YOUR CREDIT SCORE

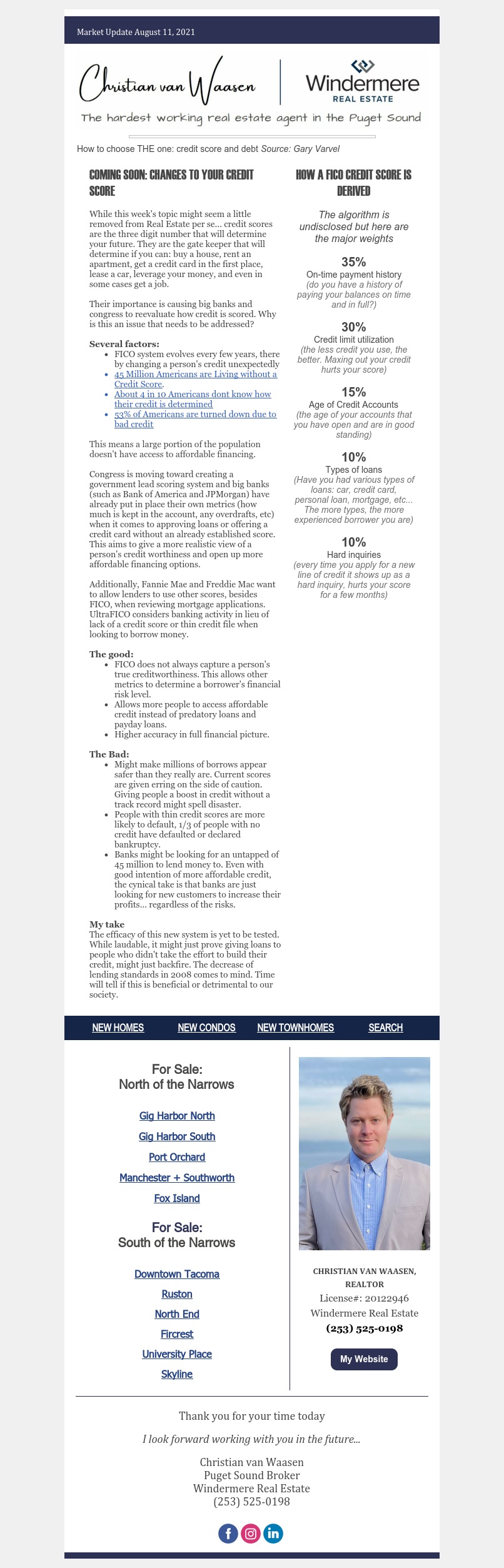

While this week’s topic might seem a little removed from Real Estate per se… credit scores are the three digit number that will determine your future. They are the gate keeper that will determine if you can: buy a house, rent an apartment, get a credit card in the first place, lease a car, leverage your money, and even in some cases get a job.

Their importance is causing big banks and congress to reevaluate how credit is scored. Why is this an issue that needs to be addressed?

Several factors:

- FICO system evolves every few years, there by changing a person’s credit unexpectedly 45 Million Americans are Living without a Credit Score.

- About 4 in 10 Americans dont know how their credit is determined 53% of Americans are turned down due to bad credit

- This means a large portion of the population doesn’t have access to affordable financing.

Congress is moving toward creating a government lead scoring system and big banks (such as Bank of America and JPMorgan) have already put in place their own metrics (how much is kept in the account, any overdrafts, etc) when it comes to approving loans or offering a credit card without an already established score. This aims to give a more realistic view of a person’s credit worthiness and open up more affordable financing options.

Additionally, Fannie Mae and Freddie Mac want to allow lenders to use other scores, besides FICO, when reviewing mortgage applications. UltraFICO considers banking activity in lieu of lack of a credit score or thin credit file when looking to borrow money.

The Good:

- FICO does not always capture a person’s true creditworthiness. This allows other metrics to determine a borrower’s financial risk level.

- Allows more people to access affordable credit instead of predatory loans and payday loans.

- Higher accuracy in full financial picture.

The Bad:

- Might make millions of borrows appear safer than they really are. Current scores are given erring on the side of caution. Giving people a boost in credit without a track record might spell disaster.

- People with thin credit scores are more likely to default, 1/3 of people with no credit have defaulted or declared bankruptcy.

- Banks might be looking for an untapped of 45 million to lend money to. Even with good intention of more affordable credit, the cynical take is that banks are just looking for new customers to increase their profits… regardless of the risks.

My Take:

The efficacy of this new system is yet to be tested. While laudable, it might just prove giving loans to people who didn’t take the effort to build their credit, might just backfire. The decrease of lending standards in 2008 comes to mind. Time will tell if this is beneficial or detrimental to our society.